The focus these days is on the amount of debt in the Chinese financial system. Few economists are looking at the data on bad debt from the court system. The data includes numbers on private lending, bank and other financial institution lending, and credit card debt.

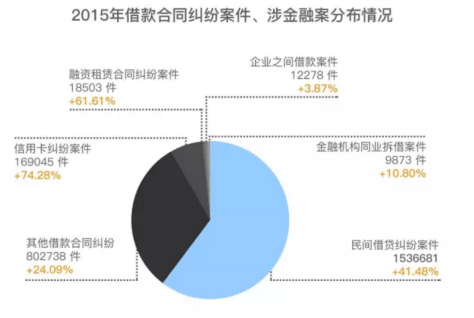

The data on lending disputes is partially useful, because it sets out numbers and percentage increases, but does not set out total amounts in disputes. The pie chart above sets out data on different types of lending and finance sector disputes.

The data on lending disputes is partially useful, because it sets out numbers and percentage increases, but does not set out total amounts in disputes. The pie chart above sets out data on different types of lending and finance sector disputes.

Private lending

This category encompasses a range of non-financial lending, from simple notes between individuals to P2P lending. Zhou Qiang’s report stated that 1,420,000 private lending disputes were resolved in 2015, with total amounts in dispute of 8,207,500,000,000 RMB (1,259,620,865.48 US Dollars. This latest report states 1,536,681 new private lending cases were accepted, up 41.48%, but does not set out the amounts involved.

The total amounts in dispute are likely greater–greater work is required to tease out the details, as to how much of it is attributable to P2P lending, and other forms of business-related lending. Recent studies by local courts reiterate that these cases often involve fuzzy lines between companies and their owners, multiple guarantees or quasi-guarantees.

Bad debt cases involving financial institutions

Financial institution call loans: 9873, up 10.8%, inter-company loans: 12278 cases, up 3.87%, other types of financial loans (loans by financial institutions): 802,738, up 24%. Finance leasing disputes: 18,503 cases, up 61%, credit card disputes: 169,045, up 74%, insurance, guarantee, pawn shop lending disputes, up 15% and more.

It is likely that the SPC has more data about specific types of disputes in the finance sector, such as wealth management products, but this report did not set out that level of detail.

Using the SPC’s and other databases, further information can be obtained on the different type of loans categorized above, including security for these loans, amounts, geographies, and reasons for default.

One thought on “Big data from the Supreme People’s Court on bad debt”